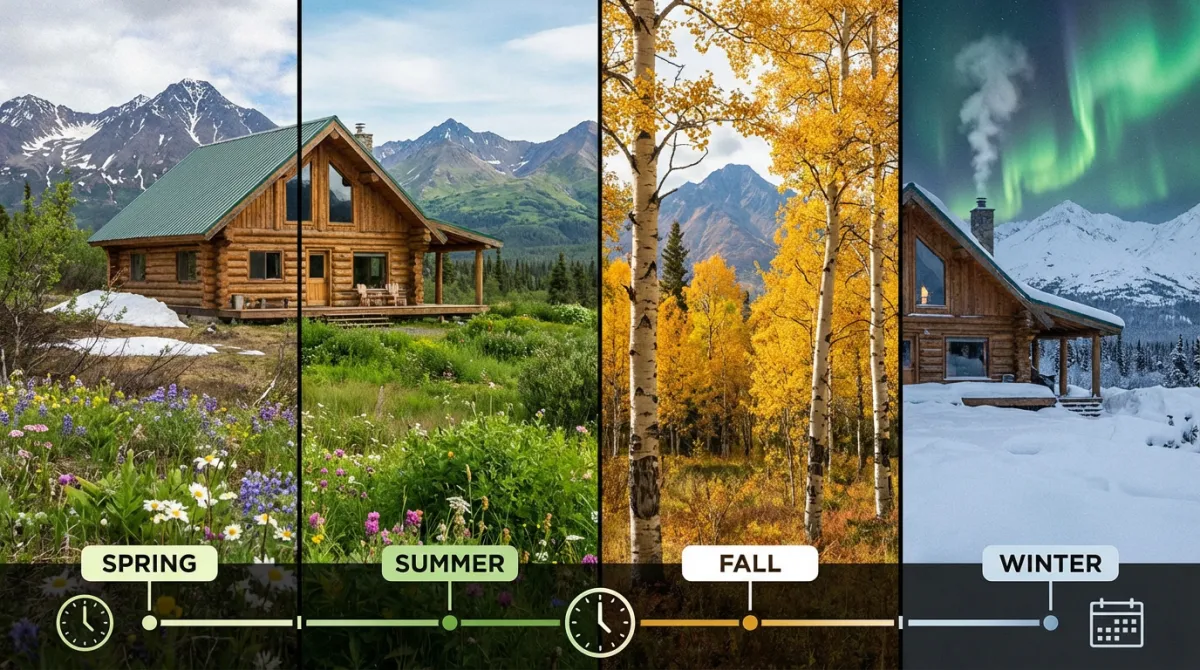

Best Time to Buy a Home in Alaska

Timing a home purchase is tricky anywhere, but in Alaska, it matters more than most places. The state’s extreme seasonal swings don’t just affect your comfort level during house tours — they fundamentally change inventory levels, pricing, competition, and even what you can learn about a property during an inspection. Unlike the Lower 48, where seasonal market differences are measured in single-digit percentages, Alaska’s market can shift dramatically between July and January.

This guide breaks down the seasonal dynamics of Alaska’s housing market so you can decide when to start your search — and more importantly, when to start your pre-approval process.

The Big Picture: Alaska’s Market Calendar

Alaska’s housing market runs on a seasonal cycle that’s more pronounced than almost any other state. Here’s the year at a glance:

| Season | Months | Inventory | Competition | Prices | Best For |

|---|---|---|---|---|---|

| Early Spring | March–April | Rising | Low–Moderate | Moderate | Early movers, deal-seekers |

| Peak Summer | May–August | Highest | High | Highest | Maximum selection |

| Fall | September–November | Declining | Low | Softening | Negotiators |

| Winter | December–February | Lowest | Lowest | Lowest | Budget buyers |

Each season brings distinct advantages and trade-offs. The “best” time depends on whether you’re optimizing for selection, price, competition, or inspection visibility.

Spring (March–May): The Sweet Spot for Prepared Buyers

Spring is when Alaska’s real estate market wakes up. Snow begins to melt, daylight hours extend rapidly, and sellers who’ve been waiting all winter start listing their homes. Inventory climbs week over week from March through May.

Why Spring Works

- Growing inventory without peak competition. Listings are increasing, but the full summer rush of buyers hasn’t arrived yet. You may have less competition for the homes you’re interested in compared to June or July.

- Motivated sellers. Homeowners who list in March or April are often eager to sell. They’ve made the decision to list ahead of peak season, which can signal flexibility on price or terms.

- Partial visibility. As snow melts, you can start evaluating landscaping, drainage patterns, and yard condition — things that are invisible under deep winter snow. By late April or May, most properties in Anchorage and the Mat-Su Valley are snow-free enough for a meaningful exterior evaluation.

- Pre-summer positioning. Buyers who are pre-approved and actively shopping in April can often lock in a home before the June–July bidding wars begin.

The Catch

Early spring means some properties still have snow cover, particularly at higher elevations (Hillside, parts of Eagle River) or in interior communities like Fairbanks. You may not get full visibility of the roof, foundation perimeter, or drainage until May. Include inspection contingencies that account for seasonal limitations.

When to Start Pre-Approval for Spring Buying

If you want to buy in April or May, start the pre-approval process in February or early March. Pre-approval typically takes a few days to a couple of weeks depending on your financial situation, and the letter is usually valid for 60–90 days. Starting in February gives you a valid pre-approval through the spring buying window.

Summer (June–August): Maximum Inventory, Maximum Competition

Summer is the peak of Alaska’s housing market. This is when the most homes are listed, the most buyers are active, and the most transactions close. If you want the widest selection, summer is your season.

Why Summer Works

- Maximum inventory. More homes are on the market from June through August than any other time of year. If you have specific neighborhood, school district, or property requirements, summer gives you the best odds of finding a match.

- Full property visibility. No snow, full daylight (up to 19+ hours in Anchorage), and green landscaping mean you can evaluate everything — roof condition, yard drainage, driveway access, outbuildings, well and septic components, and the overall lot.

- PCS arrivals. Military families arriving at JBER and Fairbanks installations during PCS season (May–August) create additional demand but also additional supply as departing families sell their homes.

- Lender and contractor availability. The real estate ecosystem runs at full capacity during summer, with faster appraisal turnaround times and easier access to inspectors and repair contractors.

The Catch

Competition is real. Desirable homes in popular neighborhoods — South Anchorage, Eagle River, newer subdivisions in the Mat-Su Valley — can attract multiple offers within days of listing. Bidding wars, while not as intense as they were in 2021–2022, still happen during peak summer months.

Prices are also at their seasonal peak. You may pay 3–5% more for a comparable home in July than you would for the same home in November. On a $450,000 purchase, that’s $13,500–$22,500 in additional cost.

When to Start Pre-Approval for Summer Buying

For a June or July purchase, start pre-approval in March or April. This gives you time to compare lenders, explore AHFC programs, and have a valid letter ready when summer listings hit the market.

Fall (September–November): The Negotiator’s Window

Fall is when Alaska’s housing market begins to cool — in both temperature and transaction volume. Buyers who missed the summer rush or who are patient enough to wait can find opportunities that simply aren’t available in June.

Why Fall Works

- Less competition. Many buyers pause their search after Labor Day, either because they’ve already purchased, moved into rentals, or decided to wait until next spring. Fewer buyers means more negotiating power for those still shopping.

- Motivated sellers. Homes that haven’t sold during the prime summer window are often still on the market because they were overpriced, had condition issues, or simply didn’t attract the right buyer. Sellers who are still listed in October know that winter is coming and may be more flexible on price, closing costs, or repair concessions.

- Price softening. Listing prices tend to ease in fall. Sellers who started high in June may reduce by September or October. Data across Alaska markets suggests fall sale prices typically run 2–4% below summer peaks.

- You experience early winter. Buying in October or November means you get a preview of what the home feels like as temperatures drop. You can evaluate heating performance, window insulation, and how well the driveway and walkways handle early snow and ice.

The Catch

Inventory is shrinking. The wide selection of summer is gone, and new listings slow to a trickle by November. You’ll have fewer options, and the home you want may not be available. Exterior inspections become more limited as snow begins to cover the ground, particularly in Fairbanks and interior communities where winter arrives earlier.

When to Start Pre-Approval for Fall Buying

For a September or October purchase, start pre-approval in July or August. If you’re currently shopping in summer and haven’t found the right home, your pre-approval from spring may still be valid — check with your lender about extensions.

Winter (December–February): Deals for the Bold

Winter is the contrarian’s buying season in Alaska. Conventional wisdom says don’t buy in winter. That’s exactly why it can work for buyers willing to accept the trade-offs.

Why Winter Works

- Least competition. Very few buyers are actively house-hunting in December and January. If a home you like has been sitting since fall, you may be the only interested buyer.

- Motivated sellers. Anyone still on the market in winter is typically highly motivated. Life events — divorce, job relocation, financial pressure — don’t wait for summer. These sellers may accept below-asking offers or generous concessions.

- Lowest prices. Winter sale prices in Alaska are typically 4–7% below summer peak prices. On a $400,000 home, that’s $16,000–$28,000 in potential savings.

- Real-world winter experience. You’ll see exactly how the home performs in Alaska’s harshest conditions. How warm is it? How much does heating cost? Can you get in and out of the driveway after a storm? These are things summer buyers can only estimate.

The Catch

The drawbacks are significant and shouldn’t be minimized:

- Very limited inventory. You’re choosing from the smallest pool of listings all year. You may not find the right home in your target neighborhood.

- Snow-covered exteriors. Yards, foundations, roofing details, drainage patterns, and landscaping are buried under snow. You may be unable to fully evaluate the property’s exterior condition.

- Frozen ground. Well and septic inspections can be more challenging (or impossible) in frozen conditions. Some inspection elements may need to be deferred with contractual protections.

- Shorter days. In Anchorage, December daylight drops to roughly 5.5 hours. Showings happen in the dark, which makes it harder to evaluate natural light, views, and exterior details.

- Appraisal complications. In rural areas, winter appraisals can take longer and may be more difficult if comparable sales are limited and access is restricted by weather.

Winter buying isn’t for everyone, but for budget-conscious buyers with flexible timelines and strong inspection contingencies, it can yield meaningful savings.

When to Start Pre-Approval for Winter Buying

For a December or January purchase, start pre-approval in October or November. Having your financing lined up before the holiday season ensures you can move quickly if the right opportunity appears.

How Alaska’s Seasons Compare to the Lower 48

In most of the continental United States, seasonal market variations exist but are relatively mild — perhaps a 5–10% swing in inventory and a few percentage points in price between peak and off-peak seasons. Alaska’s swings are amplified by factors unique to the state:

- Extreme weather. When it’s -30°F in Fairbanks, almost nobody is house-hunting. That level of seasonal demand suppression doesn’t happen in Dallas or Denver.

- Daylight variation. Alaska goes from 19+ hours of daylight in June to under 6 hours in December. That directly affects showing schedules, open house attendance, and buyer energy.

- Military PCS cycles. The concentration of military buyers entering and leaving the market on a May–August cycle amplifies the summer demand spike.

- Construction season. New homes can only be built during a limited construction season (roughly May–October). New construction listings cluster in late summer and fall.

- Road access. Some rural properties are only accessible during certain seasons, which eliminates them from the winter market entirely.

These factors create a more dramatic seasonal curve than you’ll find in any other state. Understanding this curve is a genuine competitive advantage.

Down Payment and Program Timing

Your purchase timeline also affects which programs are available to you. A few timing considerations:

- AHFC programs are available year-round, but if demand for AHFC-rate loans spikes in spring, processing times can increase. Applying during the quieter winter months may result in faster processing.

- PFD as a down payment boost: If you’re planning to use your Permanent Fund Dividend as part of your down payment, PFDs typically arrive in October. A winter purchase aligns well with using your PFD funds.

- Down payment assistance programs may have annual funding limits. Programs funded at the start of a fiscal year can sometimes run low by late in the year. Check availability early.

- USDA loan eligibility doesn’t change seasonally, but if you’re buying in a USDA-eligible rural area, winter access limitations can complicate the appraisal process.

The Bottom Line: When Should You Buy?

There is no universally “best” time. But here’s a framework:

- If you want the most choices: Buy in June or July. Accept that you’ll pay peak prices and face competition.

- If you want the best deal: Buy in November through February. Accept limited inventory and snow-covered inspections.

- If you want the best balance: Buy in late April through early June. Inventory is growing, competition hasn’t fully arrived, and you get solid property visibility as snow melts.

- If you’re on a military PCS timeline: You may not have a choice. Get pre-approved before you arrive in Alaska, and have your agent start lining up showings for your first week on the ground.

Regardless of when you buy, the pre-approval process should start two to three months before your target purchase date. That gives you time to compare lenders, explore AHFC programs, and have a valid pre-approval letter ready when you find the right home.

Ready to start? Get pre-approved now so you’re positioned to move when the timing is right — whether that’s this spring or later this year.

Get Pre-Approved with Premier Mortgage →

Frequently Asked Questions

Is winter a good time to buy a home in Alaska?

Winter can be an excellent time to buy because there is less competition from other buyers. Sellers who list during winter are often highly motivated, and you may have more negotiating leverage. The tradeoff is that snow cover can hide exterior issues, making a thorough inspection even more important.

When do the most homes go on the market in Alaska?

Listing activity in Alaska picks up in March and peaks from April through July. Summer brings the highest inventory, longest daylight hours for showings, and the best conditions for inspecting a property’s exterior and land. However, more inventory also means more competition from other buyers.

Should I get pre-approved before looking at homes in Alaska?

Absolutely. Pre-approval tells you your exact budget and shows sellers you are a serious buyer. In Alaska’s competitive spring and summer market, homes in desirable neighborhoods receive multiple offers quickly. A pre-approval letter from a local Alaska lender gives you a significant advantage over buyers who have not started the financing process.

Does the Alaska housing market slow down in fall?

Yes, market activity declines from September through November as shorter days and colder weather reduce both listings and buyer traffic. This slowdown can work in a buyer’s favor — less competition, potentially lower prices, and sellers who want to close before the deep winter months.

How long does it take to close on a home in Alaska?

Most Alaska home purchases close in 30 to 45 days from the time an offer is accepted. VA and USDA loans may take slightly longer due to additional appraisal and underwriting requirements. Factors like appraisal delays, title issues, or complex property conditions in rural areas can extend the timeline.

Ready to Make Your Move?

Get pre-approved for your home loan first — it gives you a competitive edge. Need a listing agent? We can help.

Or email contact@akhomehq.com

Disclaimer: This article is for informational purposes only and does not constitute financial, mortgage, legal, or tax advice. Interest rates, loan programs, eligibility requirements, and fees are subject to change without notice and may vary based on your individual circumstances. Alaska Home HQ is not a lender, broker, or financial institution. All loan applications are processed by Premier Mortgage (NMLS: 1168048). We may have a business relationship with Premier Mortgage and may receive compensation when you use their services through our links. Consult a licensed mortgage professional before making financial decisions. Terms of Service · Privacy Policy